Despite ongoing efforts by motor carriers to lower their insurance premiums, the majority are still experiencing increases in their insurance costs. A new report highlights the necessity for a more comprehensive approach.

A recent study focused on how rising insurance costs impact trucking fleets indicates that, despite various strategies employed to reduce premiums, most motor carriers encountered escalating insurance expenses.

The American Transportation Research Institute (ATRI) reports that fluctuating and rising insurance premiums are a significant concern for the industry. Their Analysis of the Operational Costs of Trucking reveals that insurance costs per mile surged by 47% over the past decade, increasing from 5.9 cents to 8.7 cents.

According to ATRI’s new report, “The Impact of Rising Insurance Costs on the Trucking Industry,” nearly all motor carriers saw notable increases in insurance costs between 2018 and 2020, despite efforts such as reduced coverage, higher deductibles, and improved safety measures.

All fleet sizes experienced premium increases, with small fleets paying over three times more per mile compared to very large fleets. Additionally, small fleets are consistently charged more than double the premium per mile of large fleets, which in turn pay nearly double what very large fleets do, as reported by ATRI.

Small fleets face higher insurance premiums than large fleets.

About one-third of survey respondents indicated they had to reduce wages or bonuses due to increasing insurance costs. Moreover, 22% curtailed investments in equipment and technology, which raises potential concerns about safety and driver shortages in the future.

Nonetheless, short-term crash data reveals that carriers who raised their deductibles or reduced coverage were generally more motivated to lower crash rates in the following year.

The report also outlines a method for calculating the “Total Cost of Risk” to assess the impact of escalating insurance costs on a carrier’s long-term safety and financial health, including investments in driver safety, programs, and technologies.

Reasons for Rising Trucking Insurance Costs

From 2009 to 2018, the frequency and severity of truck-related crashes increased, but the rate at which insurance costs rose during this time far outpaced the nominal increase in crash rates.

Legal issues also place financial strains on insurers, which are subsequently passed on to carriers. This is not limited to high-stakes “nuclear verdicts.” ATRI’s report on small verdicts reveals that such cases have resulted in average payments between $406,386 and $449,792.

Some economic factors within the insurance industry have also contributed to increased premium rates. From 2015 to 2019, incurred losses for commercial vehicle insurers grew annually, culminating in a 50% rise. These losses correspond with a general increase in claims, even though premiums have consistently risen at a higher rate. Consequently, some insurers have exited the market, while others are limiting coverage options.

“ATRI’s research aligns with the Triple-I’s findings regarding rising insurance costs and social inflation, highlighting that litigation and other factors significantly boost payouts made by insurers,” remarked Dale Porfilio, chief insurance officer of the Insurance Information Institute. “External influences beyond carrier safety compel increases in commercial trucking insurance costs, which in turn necessitate redesigning business strategies. Ultimately, higher premiums tend to be reflected in elevated prices for goods and services for consumers.”

Trucking Fleets’ Responses to Rising Insurance Rates

The report indicates that the primary strategy for motor carriers facing escalating insurance rates is to lower coverage levels above $1 million, particularly among very large fleets. While this can result in short-term savings on premiums, it may heighten exposure to catastrophic verdicts.

Another method to mitigate premium costs is to raise deductibles, which increases potential out-of-pocket expenses. By taking on a larger share of losses per incident, carriers can achieve lower premiums; however, small fleets often find such options unavailable due to narrower profit margins and limited capital.

ATRI’s findings suggest that declines in overall coverage or increases in deductibles are unlikely to result in significant premium reductions, unless the changes are considerable or aligned with other specific carrier or policy adjustments.

Adoption of Safety Technologies

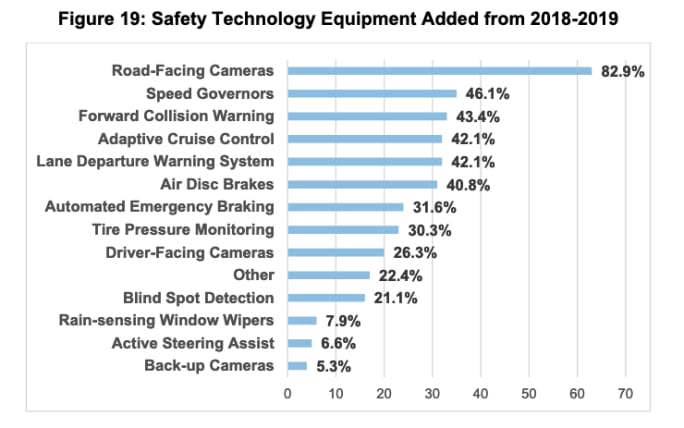

ATRI reported that 92% of respondents have incorporated new safety technologies over the past three years, with 56% integrating three or more. The most frequently adopted technology includes road-facing cameras, followed by speed governors and forward-collision warnings. However, no significant correlation was identified between newly adopted safety technologies and changes in insurance premiums.

Forward-facing cameras serve as a strategic asset for addressing insurance costs.

Road-facing cameras have become a critical resource for insurers, carriers, and drivers, offering solid safety documentation that helps minimize claims and associated defense costs. Other safety technologies indirectly affect insurance premiums; theoretically, they could lead to lower rates by reducing crashes, yet they do not yield direct improvements in premiums.

Experts in the insurance industry suggest that the overall commitment by carriers to adopt safety technology is more crucial than focusing on specific technologies. This investment signals a carrier’s dedication to reducing crashes and prioritizing safety proactively.

In conclusion, ATRI’s findings indicate that carriers should encompass all safety-related expenses, alongside insurance, as part of their total cost of risk strategy. This approach enables better long-term organization of costs and highlights the interplay between safety and various financial elements.

The complete report can be accessed through ATRI’s website.

Note: An earlier version erroneously reported the increase in insurance costs from 59 cents per mile to 78 cents per mile; the correct figures are an increase from 5.9 cents to 8.7 cents.